Why retail banks use econometrics to model behavior and risk

Analytical Alley Team

Marketing Analytics Experts

Can you predict a deposit flight or a loan default before it impacts your balance sheet? Econometric modeling provides B2C banks with a mathematical framework to quantify consumer behavior, allowing y...

Can you predict a deposit flight or a loan default before it impacts your balance sheet? Econometric modeling provides B2C banks with a mathematical framework to quantify consumer behavior, allowing you to turn complex economic signals into actionable strategy and predictive decision-making.

For CMOs and CFOs in the banking sector, these models represent the bridge between raw data and commercial outcomes. By isolating the impact of interest rates, marketing spend, and macro conditions, you can move from reactive reporting to a proactive stance that identifies growth opportunities and mitigates risk before they materialize.

Predicting customer actions with discrete choice models

In retail banking, the most critical questions often have binary answers. You need to know if a customer will churn, take out a mortgage, or default on a loan. Econometricians use Logit and Probit models to estimate the probability of these specific actions by analysing non-linear relationships in customer data.

These models analyse factors such as fee structures, income levels, and digital banking usage to determine what triggers a specific behaviour. For instance, research from J.D. Power indicates that clarity on fees can boost customer satisfaction by 4% to 5%. Logit models allow you to quantify how much a specific fee change might increase the probability of account closure across different segments, helping you balance revenue with customer retention.

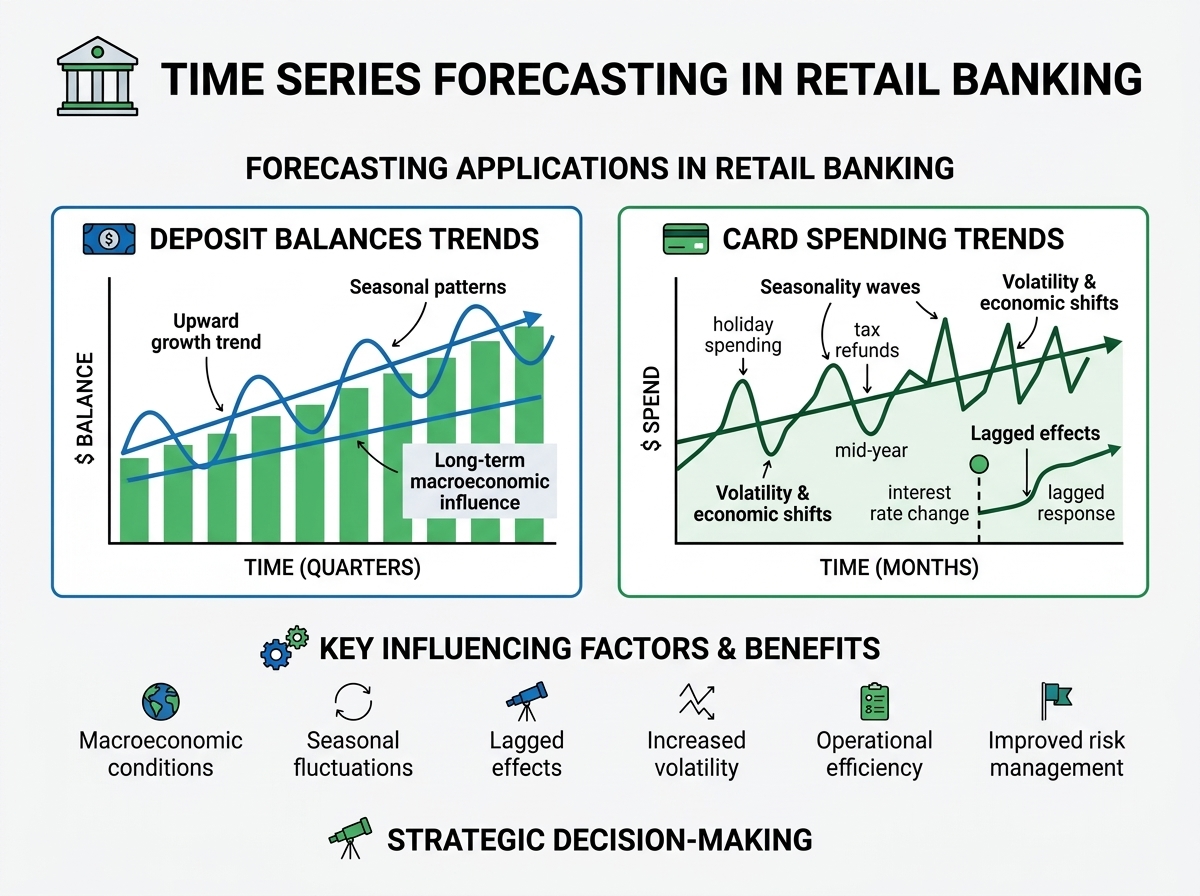

Forecasting trends with time series analysis

Retail banking is highly sensitive to time-bound fluctuations. Whether you are forecasting deposit volumes or credit card spending, Time Series Models such as ARIMA or VAR are essential for capturing trends and seasonality across the European market.

These methods account for:

By understanding these patterns, banks can manage balance sheet liquidity more effectively. This is particularly relevant as household cash flow comfort fluctuates under savings pressure, a trend noted in recent Deloitte consumer pulses.

Optimizing rates through price elasticity

Finding the "sweet spot" for interest rates is a delicate balancing act between maintaining profitability and driving customer acquisition. Price elasticity models measure how sensitive your customers are to changes in APRs or deposit rates.

The formula for elasticity is typically expressed as:

$$ epsilon = frac{% Delta text{Demand}}{% Delta text{Price}}$$

In a competitive market, even a small adjustment can lead to significant shifts in market share. Analysis of credit card pricing shows that large issuers often charge 8% to 10% higher APRs than smaller banks. Econometric analysis helps you determine if your brand equity justifies such a price premium or if a rate cut is required to stimulate loan demand in a cooling economy.

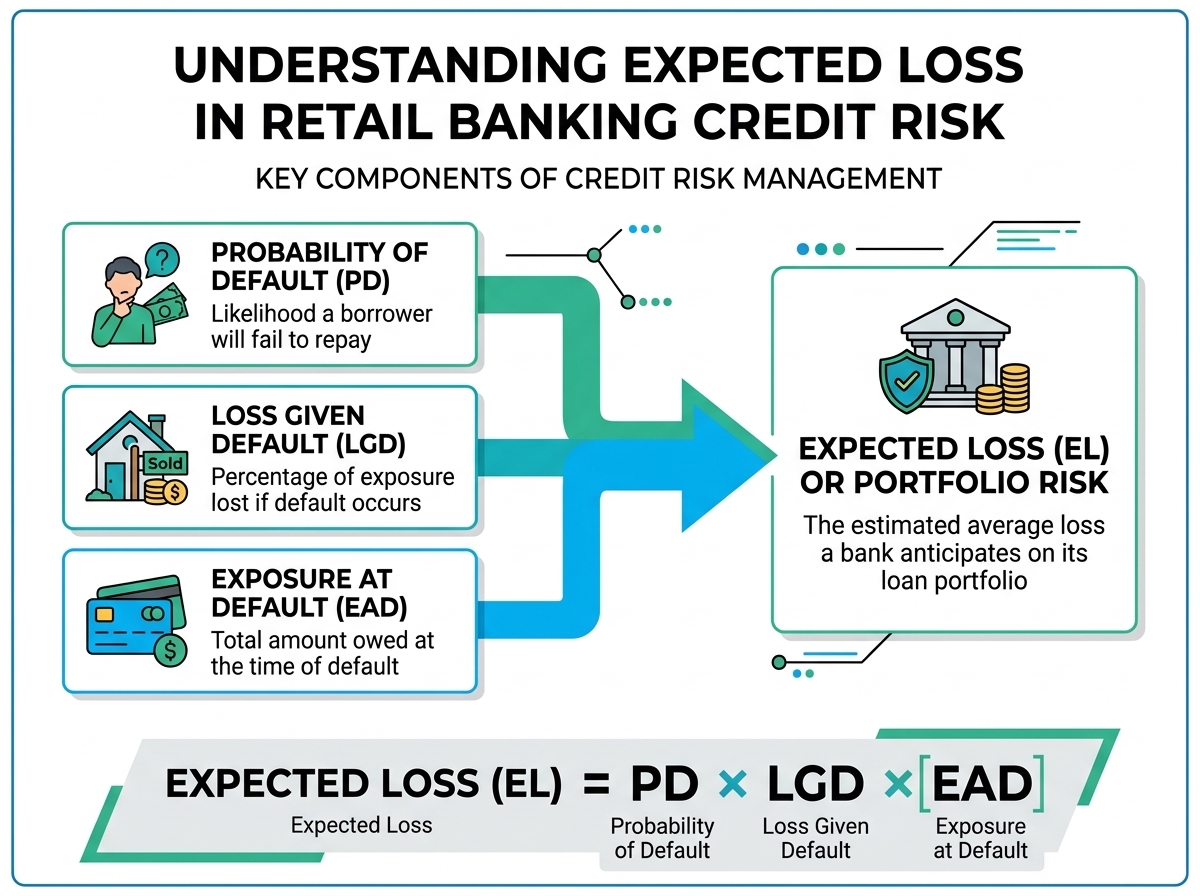

Quantifying credit risk and expected loss

Credit risk modeling is the most mature application of econometrics in banking. To manage portfolios for cards, loans, or mortgages, banks calculate expected loss using three primary components that transform individual borrower data into a portfolio-wide risk assessment.

Top-tier institutions use these econometric frameworks to refine their approvals and pricing. Implementing robust PD and LGD models has been shown to reduce non-performing loans (NPLs) by up to 10%, which can free up hundreds of millions in capital for further investment or lending.

Integrating econometrics into marketing strategy

While risk and pricing are often handled by finance teams, marketing strategists benefit immensely from these same econometric principles through marketing mix modeling. This approach moves beyond granular attribution to look at the total impact of your investments.

By applying multivariable regression, you can isolate the ROI of marketing spend from baseline business driven by brand heritage or interest rate environments. This prevents double counting conversions and ensures your marketing spend optimisation is based on incremental growth rather than organic trends.

To build an accurate model, you must ensure your data requirements for econometrics are met. This typically requires at least two to three years of historical data to account for economic cycles and the deep seasonality inherent in B2C banking.

Achieving 90% prediction accuracy

Econometric models transform raw consumer patterns into a roadmap for growth and risk mitigation. By moving beyond simple attribution and embracing aggregate data analysis, B2C banks can navigate volatile markets with confidence and clarity.

Analytical Alley helps European organizations apply these sophisticated models to slash ad waste by up to 40% and predict business outcomes with over 90% accuracy. If you are ready to see how econometric modeling can optimise your media strategy and customer acquisition, explore our case studies or book a demo to see our mAI-driven approach in action.

Get Marketing Analytics Insights

Monthly briefings on marketing mix modeling, budget optimisation and what's actually moving the needle for European brands.